Whether one is headed into or in retirement already, there are countless financial articles advising that one should reduce the risk in the portfolio’s. One way to achieve this is to increase our weighting in our portfolio to bonds and income bearing vehicles. Many suggest that we increase our fixed income exposure at 65 (average retirement age) to 50-70%. Many retirees look towards their bonds to provide lower risk and provide a consistent income stream. The problem with this concept is that fixed income at 50-70% of your portfolio may no longer be the optimal asset mix. Case in point is that bond funds and indexes are now losing money, the Canadian Bond Index lost approximately 3% in the 2021 calendar year (Source: Bloomberg Morningstar Core Canadian Bond Index) and so far in 2022 the same index is down 3.33% at time of writing (Source: Bloomberg Morningstar Core Canadian Bond Index). So, is there a way to get fixed income like security without the constant volatility in risk witnessed in the stock markets and now the fixed income markets (read the last paragraph)?

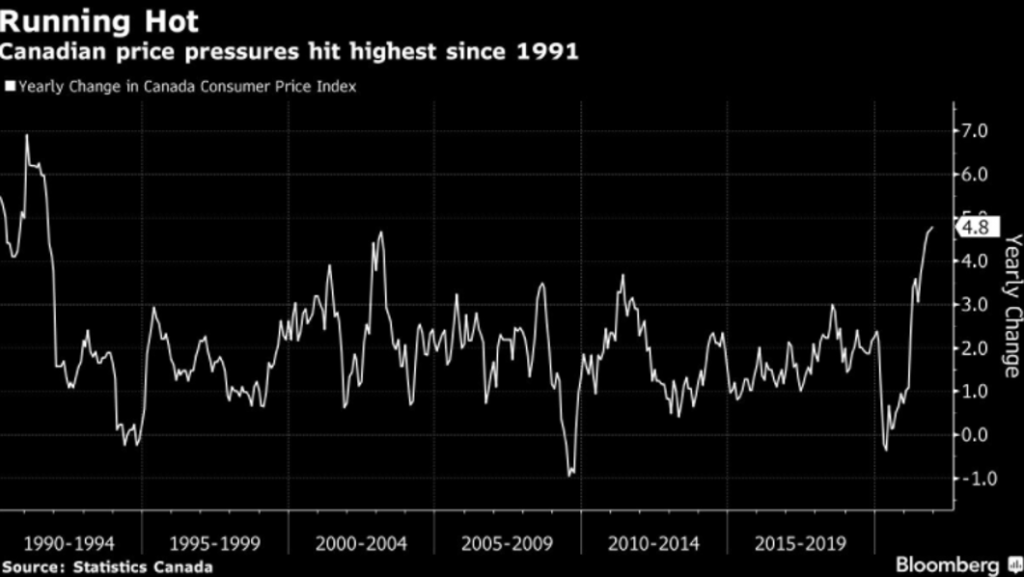

Bonds can work against your portfolio at certain points of the market cycle. Take for example an environment where inflation starts to increase (i.e. economy growing at a healthy clip of 5% or more per annum or in a situation that we face today where an economy that has been supported by government spending and monetary stimulus – reducing interest rates) and in US the inflation reached 7%+ and in Canada 4.8% in 2021. These numbers represent the fastest year over year increases since the late 1970’s.

So, how does the Fed and the Bank of Canada tame inflation? They start the path of increasing rates. The Bank of Canada will meet on January 26th and the bond market does expect a higher probability of them starting to raise rates 25 bps then. The Fed should start in March as their CPI Index has now reached a 7 handle.

With rates increasing how does that affect your portfolio? Bonds are impacted by 3 major components, the first is duration, secondly is the rate of interest indicated on your bond and lastly the direction of rates. Let’s tackle duration first. Duration measures a bond’s sensitivity to interest rate changes expressed in years. In simplest of terms, the longer the duration, the more sensitive the bond is to interest rate moves, and more importantly the more its price will change. What should you do if interest rates are expected to increase? It is worthwhile to lower duration of your bond portfolio, to capture less of the decrease in price.

Can you explain why? Well, there is an inverse relationship between bond prices and interest rates. As rates rise, bond prices decreases. Let’s explore this concept a little further. If you currently own a 20 year bond with a coupon of 5%, and interest rates rise to 7% in one year, then new issues of bonds pay a higher rate. This makes the new 7% bond more attractive to investors and the 20 year bond of 5% less attractive. More demand on the 7% bond will push its prices higher in the market. In order to lure investors away from the 7% bond, the 5% bond needs to be discounted (price needs to decrease). More often than not, investors will sell their 5% coupon bond to purchase the 7% coupon.

The best way to manage duration and interest rate risk is to hold a diversified portfolio of different types of bonds (corporate, emerging market, high yield, commercial and MBS). But with geopolitical risk on the rise (i.e. trade tensions between China and US growing, Russia on the verge of invading Ukraine) bonds may not look as safe as its name suggests. There is another way to divest your portfolio from inflation, interest rate and market risk. Please feel free to call me at 416 882 7462 or email me at devin@dlwealthmanagement.ca to schedule a zoom meeting so we can review your current situation and provide an option for your bond portfolio with increased stability and consistency.